Table Of Content

“When the deal falls apart in escrow, you might be the only buyer who’s still interested,” she says. If you’re paying in cash, congratulations on your success and/or luck in life. Otherwise, you’ll need to save up for a mortgage agreement, and that may take time. The median sale price includes starter homes and smaller residences meant for one or two occupants, meaning it may actually understate the priciness of the LA market. The median asking price per-square-foot was $440 in November, meaning that a typical single-family home of around 2,000 square feet could be expected to retail for about $880,000.

Who Will Guide You Through the Homebuying Process?

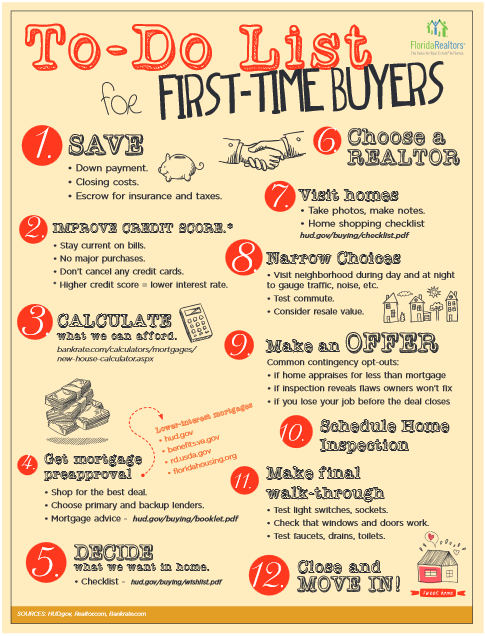

Based on your preapproval letter, your real estate agent can help you find homes within your budget. Before jumping into your home search and the homebuying process, the first step in the timeline for buying a house is to determine how much you can afford. You may have saved enough for your down payment, but don’t forget to account for closing costs, taxes, insurance, and any other unforeseen expenses that may arise when buying a house. Other closing costs can include loan origination fees, title insurance, surveys, taxes, and credit report charges.

Step 2: Get preapproved and compare loan offers (one to two weeks)

The Complete Guide to Buying a House - Business Insider

The Complete Guide to Buying a House.

Posted: Mon, 15 Apr 2024 07:00:00 GMT [source]

Your mortgage lender will calculate your debt-to-income ratio (DTI) to determine the maximum size of your loan. DTI measures how much of your gross monthly income you spend on debt. Lenders look at the money left over after your regular debts are paid to see how much you can afford for a monthly mortgage payment.

Find a real estate agent

To improve your odds of mortgage pre-approval, organize and accurately report your financial information. To determine what the lender thinks you can afford, they will look at your debt-to-income ratio (DTI). This determines how much money you have left over after paying your monthly expenses to cover the cost of a mortgage payment. Typically, lenders want your expenses to be under 28% of your monthly income, but some may approve at a higher rate.

Some you'll need to pay before you move in, and others are what you'll pay over time. A home appraisal, on the other hand, will be required by your mortgage lender to confirm that the home value is consistent with the loan amount. Even though you’ve been pre-approved for a loan, expect to provide additional documentation to your loan officer as the underwriting process progresses. Once you’ve figured out how much home you can afford, the next step is determining how much of a down payment you’ll need. There’s a lot of work to do, but don’t worry — this home buying checklist will help you roll up your sleeves and get you ready for your closing date in 10 easy steps.

Enlist The Help Of A Real Estate Professional

It’s not uncommon for homes to sell quickly and above the list price. So, don’t panic if you don’t get the first home you place an offer on. The offer should include an offer price, a deadline for the seller to respond (usually within 24 to 48 hours) and any contingencies you want to request.

The next step in the timeline for buying a house is to submit your offer as soon after touring the house as possible. Speed is of the essence in a competitive housing market with limited inventory. Talk with your agent about the terms of your deal and the competition you face to determine an offer price. You and your agent will work together to write and submit the offer letter to the seller’s agent. On your closing date the money has been exchanged and the title is now in your name. A title company or real estate attorney will close the transaction and you will typically get the keys after 5 p.m.

If you’re buying a house that’s for sale by owner (FSBO), your agent will negotiate with the seller directly. If your seller rejects your request, it’s up to you to decide how to proceed. If you have an inspection contingency in your offer letter, you can walk away from the sale and keep your earnest money deposit. Just before the closing, get updated pay stubs and other financial paperwork to prove your employment status hasn’t changed and that you’ll be able to make your mortgage payments.

What are the Tax Implications of Assuming a Mortgage?

While you have been pre-approved, you still need to meet with your lender and finalize your mortgage application. Now that you’ve completed all negotiations, it’s time to finalize and sign the purchase agreement with the seller. Once you and the seller agree on the terms, you’ll enter the closing process, which usually takes 30 to 45 days.

You can start your search by asking around for recommendations for a buyer’s agent. You can also research online for highly-rated agents and review testimonials from past clients. Be sure you’re actually getting a preapproval, not a prequalification. A prequalification could indicate that you might be approved for a mortgage but is better used to help you determine how much you might be able to afford.

A 20% down payment is typically the norm, but you can choose your own amount. Investing involves market risk, including possible loss of principal, and there is no guarantee that investment objectives will be achieved. Morgan Wealth Management is a business of JPMorgan Chase & Co., which offers investment products and services through J.P. Morgan Securities LLC (JPMS), a registered broker-dealer and investment adviser, Member FINRA and SIPC. Morgan Private Wealth Advisors LLC (JPMPWA), a registered investment adviser.

Work on making your offer appealing after finding a home you want to buy. Your offer should include the offer price, preapproval letter, and proof of funds for the down payment. Your agent will be your tour guide through the city, zeroing in on the areas that best suit your needs and budget. A seasoned agent will understand the ins and outs of the neighborhoods you want to pursue and be prepared to offer specific advice throughout the buying process.

No comments:

Post a Comment